“The one thing that’s truly future-proof is judgment.” - Gokul Rajaram

Investors today operate with unprecedented leverage. We have powerful tools and vast datasets required to distill raw information into a clear edge. The industry has standardized a level of rigour where every assumption is pressure-tested, and every output is refined with surgical precision.

Consequently, most practitioners don’t struggle to form an actionable view. Many even arrive at a genuine variant perception, that sought-after gap between the consensus narrative and reality that signals real alpha.

But while an insight identifies the opportunity, it is only the starting point.

The central challenge for investors now sits much further downstream, in the execution gap between a sound thesis and a realized return. When things go wrong now, it is rarely because the logic failed or something knowable was overlooked.

More often, the failure is an error of judgment in how a decision is carried through time.

Judgment is the endurance required to stay in the race until the payout. It is the unrelenting, daily work of sizing a position so you aren’t shaken out, updating your views without letting your ego interfere, and managing the volatility until the market finally validates your thesis.

Where Returns Actually Come From

In the past, you could win simply by knowing something others didn’t. But today, the edge of merely possessing proprietary information has largely been competed away.

We live in a world where alternative data is ubiquitous and news travels instantly. Having the information is no longer the hurdle.

The real differentiator has moved from how much data you can collect to the quality of the judgment you apply to it.

Evidence from the world of forecasting shows that piling on more inputs doesn’t lead to better results. In fact, the value of that one last data point, usually hits a wall of diminishing returns pretty quickly. The opportunity for alpha starts in making sense of the information we already have.

This is the essence of the Grossman-Stiglitz Paradox. The market stays just wrong enough to reward those of us willing to do the heavy lifting of making sense of the world. But we often overlook what this bounty pays for. It isn’t a reward for the initial “aha!” moment of a smart idea. It is the payout for the judgment required to navigate the path of that idea.

Judgment is not just what feels right or wrong. It is a specific set of actions that involves deciding how much capital to allocate, when to act, and how to respond as new information arrives. It is the continuous process of managing a living hypothesis in a noisy environment.

Without the discipline to size correctly and the presence to update as reality shifts, even the most brilliant insight remains a theoretical gain.

To close that execution gap and turn a raw insight into a realized return, we have to unpack exactly how judgment operates under pressure. In the sections that follow, the post will walk through:

What it means to have good judgment beyond just being right in hindsight.

Understanding the difference between directional bias and noise.

How behavioural firewalls protect judgment.

Real time protocol for restoring objectivity under pressure.

How to measure if your judgment is improving.

Thanks for reading. Each month, I aim to publish two in-depth company or industry analyses, alongside a couple of pieces on the principles and frameworks that guide long-term investing. If you find this work useful, I’d appreciate your subscription and a like. It helps me continue building this publication and informs what I explore next.

What Good Judgment Actually Is

We often think of judgment loosely as intelligence, experience, or even just being right in hindsight. While those elements contribute, they don’t capture how judgment functions in real decisions.

Judgment shows up in how a situation is seen, how a view is held, and how that view is adjusted as reality unfolds.

At a first principles level, it helps to think of it as a discipline with three specific parts.

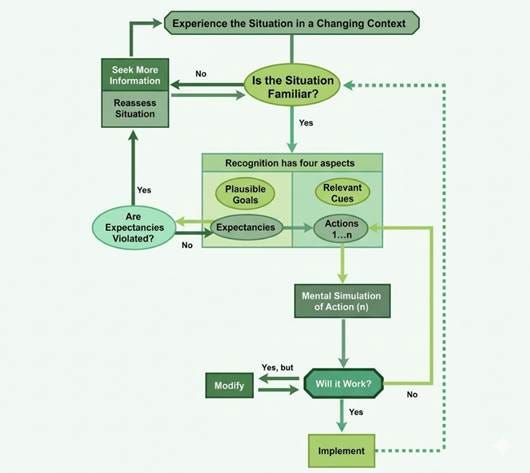

We see this consistently in fields where decisions carry real consequences. Like firefighting, aviation, emergency medicine, and military command.

Experts in these high-stakes fields are recognized less for the sheer number of options they generate and more for how quickly they orient themselves to the situation at hand.

Decision researcher Gary Klein describes this as the ability to instantly size up a situation, recognize the underlying patterns, and act based purely on the reality of the moment.

This translates well to investing.

The quality of a decision is measured by how it was made given what was knowable at the time. A well-calibrated process consistently produces better outcomes across a large sample size, even when individual results vary.

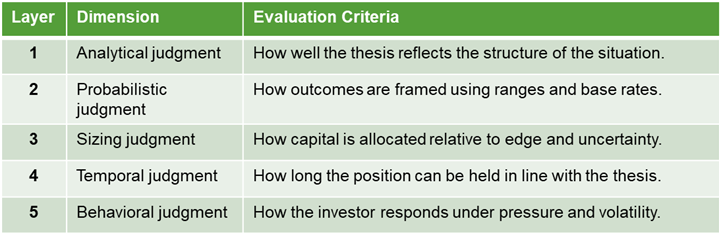

The Judgment Stack

To apply this discipline to the market, we have to recognize that judgment in investing has multiple layers. We can think of it as a stack with five distinct levels, any of which can fail independently:

Most investment failures originate in layers 3 through 5.

The initial view can be directionally sound, but poor judgment in how that view is expressed will derail the result. Position size mismatches the uncertainty. The holding period falls shorter than the thesis requires. Interim volatility provokes a response that destroys the original plan. These failures stem entirely from how the situation was handled as it evolved.

Mastering this stack is how we mitigate these failures. It reshapes how judgment itself operates.

Early on, judgment is coarse and easily destabilized. We rely on broad, loosely defined mental models that blur together under pressure, making it difficult to distinguish signal from noise when it matters most.

With deliberate practice, judgment becomes more structured and discriminating. The mind starts to encode situations in terms of relationships, patterns, and conditional responses. What once required slow, effortful analysis begins to register almost immediately.

This shift from effortful thinking to attuned judgment is what allows an investor to stay oriented as conditions change.

Instead of reacting to each new data point in isolation, judgment becomes less about constant re-evaluation and more about maintaining a coherent, adaptable view that allows for clear-headed execution under pressure.

Why Judgment Drifts

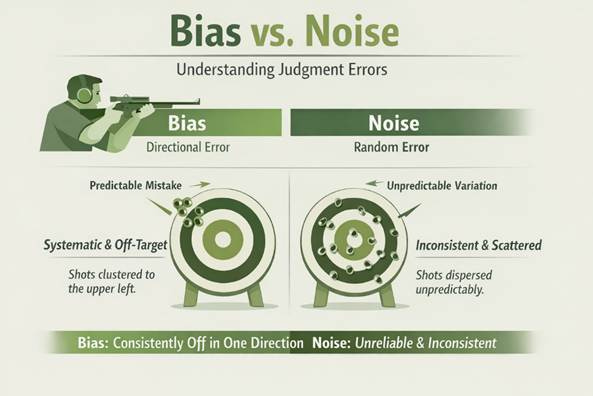

If judgment develops through experience, it should grow more consistent over time. Unfortunately, consistency is incredibly hard to achieve. To improve, we must distinguish between two very different types of error. Bias and Noise.

Think of a firing range target.

Bias is a directional error. If a shooter consistently hits two inches high and to the left, they are biased. They are predictably wrong. In investing, this is the “perma-bull” analyst who overestimates every earnings report.

Noise is unwanted variety. It is a scattered shot pattern with no shared direction. It is simply lack of consistency.

While we are highly trained to spot bias, we are often entirely blind to noise.

Daniel Kahneman illustrated this eloquently in a study of an asset management firm. They asked 42 experienced investors to independently estimate the fair value of a stock based on the exact same one-page description. The median “noise”, which is the typical gap between any two estimates, was a staggering 41%.

This variance surprises us because of a psychological quirk known as naive realism. Our own view feels internally consistent. When we encounter a very different estimate, it is natural to attribute the gap to differences in information or understanding. That 41% gap usually comes from small, invisible variations in assumptions, emphasis, and prior experience that accumulate into a large divergence in conclusions.

We must look at the total error in our judgment as the sum of both bias and noise. Reducing noise can improve accuracy just as much as reducing bias.

The Three Levels of Noise

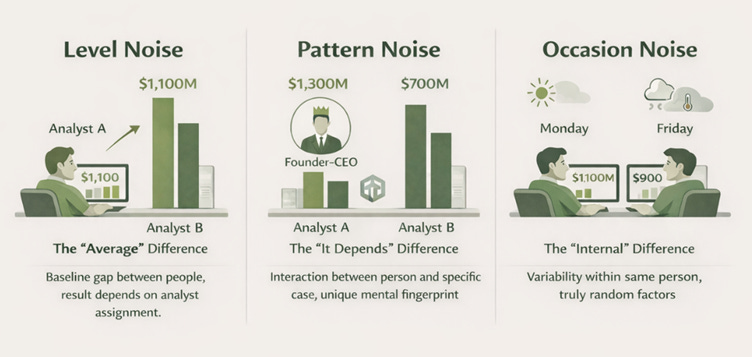

In the same body of work, Kahneman, Sibony, and Sunstein break down this system noise into three nested layers that show up constantly in investing.

Here is how those three layers look like in practice.

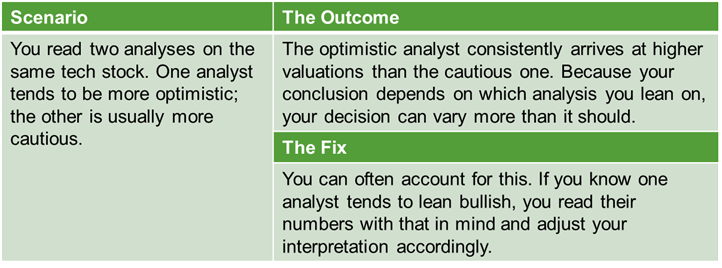

1. Level Noise

This is the baseline difference in how your judgment tends to show up.

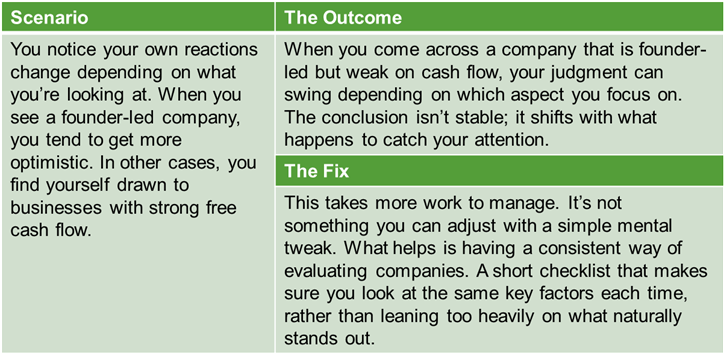

2. Pattern Noise

This is where your tendencies meet the situation, and it’s often the hardest source of inconsistency to notice.

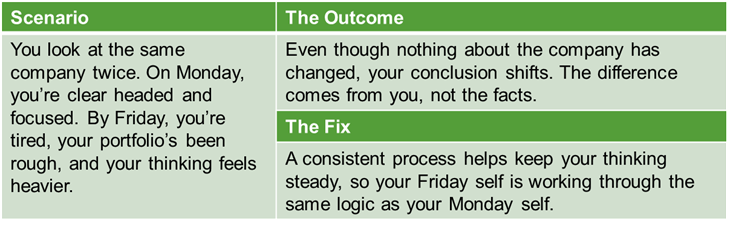

3. Occasion Noise

This is how your judgment shifts depending on the day you’re having.

What to Take From This

The confidence we feel when we’ve finally “figured it out” is just a feeling. That internal signal is simply the brain dispensing a chemical reward for reaching a conclusion. We experience that “aha!” moment just as strongly whether our judgment is centred on the bullseye or scattered 40% wide of the mark.

This leads to one of the most remarkable findings in decision science. Simple, consistent rules almost always outperform individual gut intuition in predictive tasks. A basic linear model routinely produces better results than the clinical judgment of a highly trained expert.

Even more counter-intuitive is the fact that a model of the judge beats the judge. If you take an investor’s own decision patterns and apply them consistently, without the noise of mood, health, or timing, that model will predict outcomes better than the investor themselves. It turns out that the “nuance” we think we’re adding, that subtle feeling that this time is different, is usually just noise in disguise.

The takeaway here isn’t that we should surrender our judgment to the robots.

Rather, it is about how we run our process. Since our best insights are so often tangled up with noise, the goal is to build guardrails to handle the repetitive parts of the job where we are most prone to drift.

This frees us up to focus on the complex, creative insights that a formula cannot see.

How Rules Protect Judgment

The relationship between rules, algorithms, and human judgment is widely misunderstood. The conventional framing treats them as substitutes, as if adopting a strict rule diminishes the practitioner’s skill. In reality, the opposite is true.

Behavioural science consistently shows that simple rules often outperform human judgment. The gains come almost entirely from the elimination of noise. A rule does not have a Friday Self. It is simply your best ex-ante judgment, crystallized in advance to operate without the interference of a bad mood or a stressful week.

For the investor, this insight is critical because of our biology. When a position moves violently against you, the quality of your judgment naturally slips.

This is a matter of physiology. Our cognitive resources are finite, and high-level stress consumes them. Research into our endocrine response shows that severe, prolonged drawdowns physically change how the brain processes value and risk. The same calm, rational person who sized the position disappears during a 30% turbulent drawdown.

The decision to hold a position should never be remade from scratch under these physiological conditions. A pre-committed decision rule helps as a shock absorber. We build these rules because our future, stressed-out selves simply cannot be trusted with capital in the heat of the moment. You’re protecting judgment from the parts of yourself that tend to show up at the worst possible time.

If you’re joining us for the first time, I took a deep dive into this specific phenomenon in an earlier piece, Rules Matter More Than Insight. There, I explore the data on why our biology becomes a liability during volatility and why the most successful practitioners prioritize process over brilliance. It’s a helpful foundation for what we’re discussing today.

Freeing the Mind for the Hard Choices

This approach helps channel judgment into the decisions that count.

Studies into how experts make decisions in the wild show us exactly where human pattern recognition and mental simulation remain irreplaceable.

It’s also where investing becomes less about working with clean and tidy assumptions and more about making sense of an unfolding picture. You’re trying to spot when an industry is undergoing structural change, get a feel for how a management team actually operates, or notice the early signs that competition is starting to tilt in a new direction.

Human judgment is also required at the boundaries of these rules to handle the “broken leg” exceptions. An algorithm might highly predict a person will go to the movies tonight, but if you know they just broke their leg, you override the rule.

In investing, judgment is needed in these edge cases when a specific piece of context that is not captured in the rule, materially changes the reality on the ground.

As routine work is handed over to systems and structures, your role will shift more toward deciding where attention belongs and what truly matters.

Well-chosen rules absorb the decisions most vulnerable to noise, creating the cognitive space to step back, connect the dots, and see what the data alone doesn’t clearly reveal.

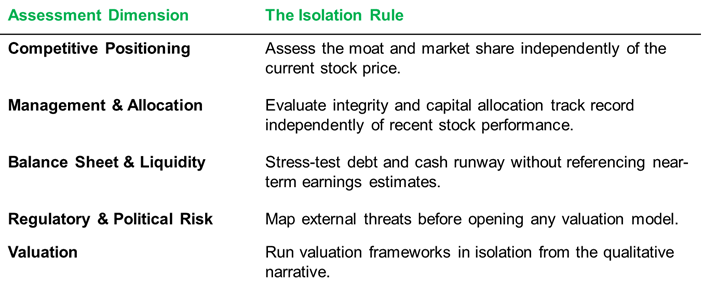

Building Firewalls

The best place to build one of these rules is right at the beginning of your research process.

As humans, the greatest vulnerability during the initial research phase is our natural desire for coherence. We are wired to leap from a few compelling facts straight to a clean, unified narrative.

You read a thoughtful proxy statement, get pulled in by the CEO’s vision, and before long the valuation starts to feel more attractive than it did before. One positive impression quickly spills over into everything else.

To guard against this, we can borrow a concept from decision science known as the Mediating Assessments Protocol. The protocol operates on one strict behavioural rule. You must build firewalls between the different dimensions of your research. You have to assess each component of a thesis completely independently before you are allowed to zoom out and form a final opinion.

To build these firewalls effectively, you must evaluate each assessment dimension as a standalone hurdle.

The discipline here is in the strict isolation. By evaluating these dimensions completely independently, you force a level of objective discipline into your routine, and avoid falling in love with a stock story.

The Judgment Loop

To bring this into your day-to-day decisions, you need something you can come back to consistently. Here is how it can be thought of in three stages.

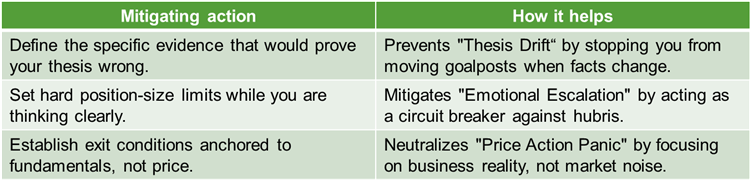

1. The Pre-Mortem

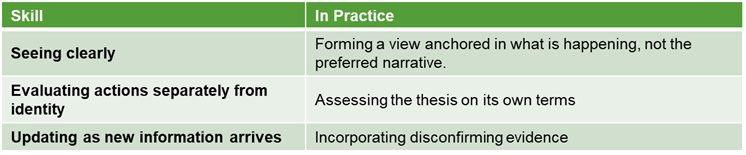

Before entering a position, spend time with how things could go wrong. Instead of asking why an idea will work, imagine a future where it hasn’t. If the position is down meaningfully a year from now, what likely happened? This forces you to define failure before you develop an emotional attachment to the thesis.

Practically, this means building structural circuit breakers that prevent your emotions from moving the goalposts once the trade is live.

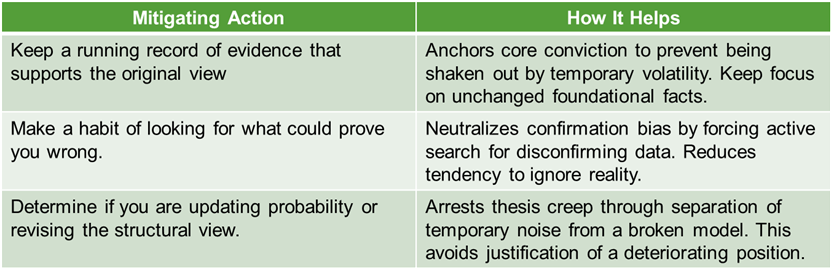

2. Active Monitoring

Once you’re in the trade, new information arrives constantly. When we own a stock, we have a massive psychological incentive to explain away inconsistencies as mere noise. Over time, this leads to a gradual reshaping of the original thesis to accommodate disconfirming evidence.

Stay grounded by systematically tracking the evidence, maintaining a clear distinction between temporary market noise and the facts that either support or shatter your original view.

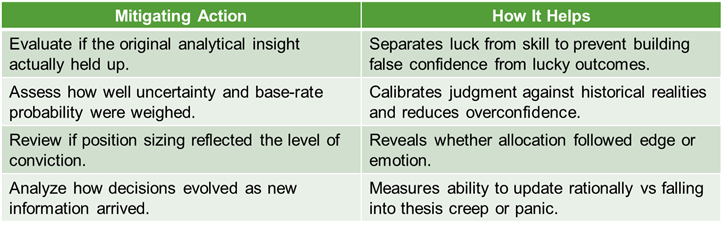

3. The Post-Mortem

When a position is closed, step back and recalibrate. Regardless of the outcome, reflect on whether the process was sound. A strong process can lead to a poor outcome through bad luck, just as a weak process can lead to a windfall through pure chance. Confusing the two triggers outcome bias and collapses your learning loop.

An effective post-mortem evaluates actions, not identity, by asking questions designed to separate a lucky windfall from a repeatable process.

There is also immense value in getting an external perspective here to surface blind spots. However, you must be selective about whose standards you internalize. You want to debrief with individuals chosen for their intellectual honesty under uncertainty and their ability to argue fairly, rather than just their intelligence or agreeability.

Why Judgment Fails

There’s a certain comfort in failing with the crowd. It spreads the pain around the herd and makes it easy to brush off.

The failure that really stings is being completely right about your idea and still losing money. That’s the tragedy of investing. It’s what happens when someone does the hard work, spots the right opportunity, but then trips over their own behaviour once they own the stock.

The fascinating part is that these mistakes aren’t random.

When you look at the biggest blow-ups in our industry, they almost always trace back to three very predictable patterns of bad judgment.

1. Being Right but Early

There is nothing quite as frustrating as having the perfect thesis but getting the timing wrong. You see the mispricing, you make the bet, but the rest of the world just hasn’t caught on yet. The market starts moving against you, not because your analysis is flawed, but simply because you are early.

In decision-making research, this is known as a failure of temporal judgment. As Klein points out, true expertise isn’t just knowing what to do. It’s the psychological stamina to know when to wait. It is incredibly difficult to maintain a stable view of a business when the immediate, daily feedback from the market is violently negative. If you get shaken out of a trade before the thesis actually plays out, it doesn’t matter how right your initial insight was. You lose anyway.

The defence against this isn’t stronger conviction, it’s better positioning.

Case Study: Jeremy Grantham and the Dot-Com Bubble

The Situation: In the late 1990s, Jeremy Grantham and GMO argued that U.S. equities, especially large-cap tech, had reached bubble valuations. They shorted the most egregious names and reallocated to cheaper assets well before the March 2000 peak.

The Judgment: This is where the rubber really meets the road in decision making. From 1998 to 2000, GMO stayed cautious while the tech bubble raged around them, leading to severe underperformance. Grantham looks back on it as a brutal period of being too early. It perfectly illustrates the danger of clashing timeframes. GMO was playing a 5 to 7 year game, but their clients were stuck in a 1 to 2 year mindset. When the firm refused to abandon their discipline and join the madness, those clients packed up and fired them.

The Lesson: This is a classic example of what happens when you try to play the long game using short-term money. Their insight into the market was spot-on, but the real error was assuming their clients had the stomach for the wait. The patient capital they thought they had just didn’t exist, and clients pulled their funds right at the finish line.

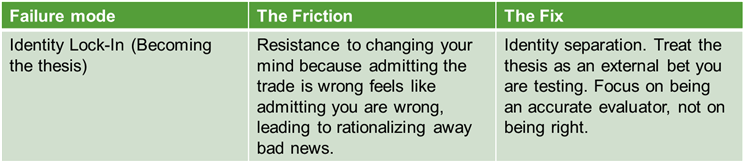

2. Identity Attachment

It’s one of the most dangerous traps in investing. Letting your portfolio become your personality. Over time, it is incredibly easy to adopt a label.

You become “The Value Guy” ,“The Tech Bull” or “The Perma-Bear”.

But the moment an investment thesis becomes intertwined with your professional identity, changing your mind stops feeling like a simple portfolio update, it feels more like a betrayal of who you are.

Daniel Kahneman and his colleagues documented exactly why this is so destructive to our judgment. When we finally piece together a complex thesis, our brain rewards us with a powerful rush of confidence.

The trap is that we process that subjective feeling as hard knowledge. We are perfectly happy to revise a temporary feeling, but we are wired to fiercely defend our knowledge. Once your brain codes a stock pick as a fact tied to your identity, any new, conflicting evidence is no longer seen as a warning sign. It’s just treated as an annoying glitch to be rationalized away.

If you can’t untangle your identity from your thesis, you lose the ability to update your views when the facts turn against you.

The defence against this isn’t trying to just be less emotional, it’s changing how you frame the job.

Case Study: Bill Ackman and Valeant Pharmaceuticals

The Situation: Bill Ackman built a massive position in Valeant Pharmaceuticals based on a sound variant perception. The market was valuing it like a normal pharmaceutical company, but Ackman correctly saw it as a highly efficient acquirer of cash flows.

The Judgment: The problem began when he launched a massive public defence of the company, tying his reputation to the mast. The Valeant thesis became completely tangled up with his identity as a visionary activist. So, when the political and regulatory weather started turning ugly, he couldn’t see it. His brain had already coded his thesis as a hard fact, making it painful to acknowledge the early warning signs.

The Lesson: This is how ego can create blind spots. The initial analysis was right, but because his identity was attached to the stock, he couldn’t update his views and change his mind when the facts changed.

The Counterfactual Case: Warren Buffett and the Airlines

The Situation: In 2016, Warren Buffett reversed a decades-long rule and bought heavily into airline stocks. His initial insight was sound. The industry had finally consolidated. But in 2020, the COVID-19 pandemic arrived and structurally destroyed the entire premise of why he owned them.

The Judgment: Buffett didn’t hesitate or try to protect his reputation. Because he hadn’t spent years publicly marrying himself to the trade, he suffered no ego damage when it broke. He cleanly exited the entire position near the absolute bottom of the market, updating his view instantly and acknowledged his mistake.

The Lesson: Great judgment isn’t static. The difference between Ackman’s Valeant and Buffett’s airlines is not superior analysis. It is the relationship each investor maintained with their thesis. To survive, you must treat your thesis as a temporary action to be tested against reality, not a permanent identity to be defended.

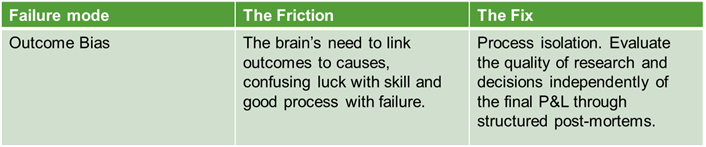

3. Outcome Bias

It is tempting to look at a winning trade and think, “I’m a genius”.

But evaluating the quality of your judgment entirely by outcome is one of the fastest ways to destroy your process over time. In behavioural science, this is known as outcome bias and in a field like investing, it is lethal.

The core problem is the massive time lag. You decide today, but the final verdict might not arrive for three to five years. By the time the payoff finally hits, the link between your original idea and the result has been completely scrambled by market noise and unpredictable variables.

But the human brain hates ambiguity and craves a clean story. So, when we win, we tend to credit it to skill even if the actual decision was reckless. When we lose, we assume our analysis was terribly flawed, even if the original logic was undeniable. Evaluating yourself this way doesn’t build true expertise, it just builds expensive superstitions.

To truly compound skill, one must completely break the link between decision making and outcome.

The defence against outcome bias requires mechanical separation.

Case Study: Tiger Global and the 2021 Crossover Boom

The Situation: Leading up to 2021, Tiger Global deployed a wildly disruptive strategy. In a world awash with cash, they realized their best advantage was speed. They wrote massive checks lightning-fast, stripped away traditional due diligence, and paid premium prices to win deals.

The Judgment: Because the initial returns were incredibly positive, the firm fell right into the outcome bias trap. They looked at the scoreboard and attributed all of that success to their brilliant new process. The time lag between their rapid investments and the ultimate reality of the market was just long enough for them to mistake a fragile strategy, subsidized entirely by a historic bubble, for pure genius. When the monetary regime shifted in 2022, the lack of a safety net was exposed, resulting in historic drawdowns.

The Lesson: This is how outcome bias destroys your judgment in a delayed-feedback environment. A successful early outcome, achieved through a highly risky process, was falsely recorded as evidence of skill. The positive feedback loop from the market was so resounding that it overrode basic risk management. It proves that if you don’t actively separate luck from process, you are highly vulnerable to being misguided.

How to Restore Judgment in Real Time

When our judgment slips, our first instinct is to try and analyze our way out of the hole. But a behavioural failure needs a behavioural intervention.

In investing, regaining your balance matters just as much as avoiding the fall. Markets never rest, and if you are busy agonizing over a bad call, you are missing the new developments unfolding around you.

You have to reclaim your objectivity and correct your lens immediately so you can respond to the new reality gaping right in front of you. If you can clear your head fast enough, you often find that navigating the new volatility is often exactly how you recoup the losses from your initial stumbles.

To actively break the spell of market pressure and get back to neutral, you need to take these steps:

Fall back on rules first. Before attempting any reassessment, prune your position size to a level that eliminates forced-exit risk. Creating cognitive space allows for clear judgment.

Separate yourself from the decision. Detach your identity from the thesis. The decision to enter the position belongs to the past. The only relevant question now is whether continued ownership is justified.

Re-anchor to reality. Return to the premises that made the thesis compelling in the beginning. Cash flows, incentives, and competitive structure. Strip away the current market price and ask what a dispassionate observer would make of the investment.

Reconstruct the thesis from scratch. Starting from current evidence, rebuild the thesis from the ground up. Ignore your entry price. If the case cannot be rebuilt to a level of conviction that justifies a fresh entry, it should be closed.

Seek disconfirming views. Solicit the most articulate bearish argument to stress test your reconstructed thesis. A thesis that cannot survive direct engagement with a sharp opposing view does not deserve your capital.

Think of this checklist as a way to get your head back in the game after your judgment has been compromised. The most dangerous investing mistakes tend not to come from a sudden lapse. They come from the deeply human habit of explaining away early warning signs piece by piece.

Running this drill forces you to stop rationalizing and start evaluating. It is your best defence against that exact trap.

The Highest Measure of Judgment

If rules and firewalls are how we protect our judgment, how do we measure if it is getting any better?

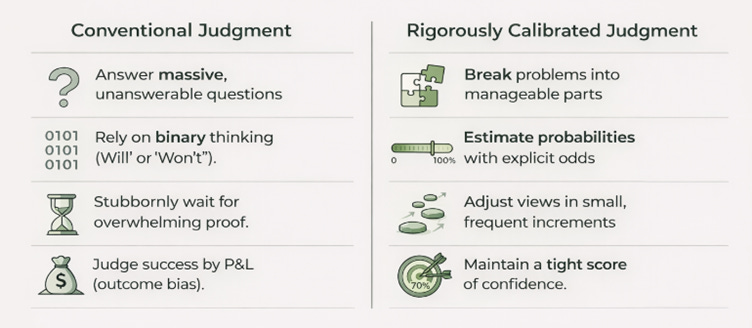

The absolute highest standard for investment judgment is a statistical discipline called calibration. It is the strict, measurable alignment between how confident you feel and how accurate you actually are over time.

When researchers study individuals with truly elite judgment, people who consistently out-predict expert consensus, they find that they operate with a rigorously calibrated mindset. They treat their judgment as an instrument that needs constant tuning, completely abandoning the standard way most of us make predictions.

This is what calibrated judgment looks like in practice:

It requires you to maintain a genuinely probabilistic relationship with your ideas, holding deep conviction and healthy uncertainty at the exact same time.

When you operate this way, intellectual honesty and measurable accountability become your default setting, changing how you manage capital.

The Final Measure

The market is entirely indifferent to your raw intelligence, your effort, or your access to management. It exclusively rewards clarity under pressure.

To survive this environment, we must maintain the continuous, daily discipline of perceiving a situation accurately and holding our behavioural coherence through the natural volatility between insight and resolution. Ultimately, the market pays you for being right in size, right in time, and right in your conduct.

Variant perception creates the opportunity. Judgment determines whether that opportunity is captured.

I’m sharing information here to educate and inform, not to provide financial or investment advice. Like any other personal financial matter, your own due diligence is paramount.

Wonderful. Thank you for the thoughtful piece and insight.