Earnings Notes (Aug 2025)

Updates across SGX:CY6U, NYSE: ARE, NYSE: ABR, NYSE: VICI, NYSE: DOCS, SGX: G13, SGX: WJP

“What gets measured gets done, what gets measured and fed back gets done well, what gets rewarded gets repeated.” - John E. Jones III

This post is a return to a few familiar names after the latest round of earnings updates, to see whether reality still rhymes with the theses set. If they hold, the names will continue to be covered; if it bends the wrong way, they will be retired. As of this review, the covered names will remain.

The backdrop is a world in flux, actively reorganizing itself. Supply routes are being rebuilt for resilience rather than speed. Energy, data, and essential services are now table stakes. Policy-making is active and the price of capital matters again. In such conditions, prediction helps less than preparation. What endures are businesses that turn day-to-day variability into dependable earnings.

With that frame, each update is parsed for the same signals. Whether utility deepens and customers return by habit. Contracts and regulation anchoring cash flows. Balance sheets that preserve optionality and not at the mercy of the clock. Managers placing capital with care and returning surplus when better uses are scarce.

Three key themes tie these names together.

Beginning with endurance, the aim of an investor is to seek out businesses where time does the work. Contracts, habits, and regulation provide the scaffolding for compounding. VICI translates leisure into long, inflation linked rents that arrive on schedule. Alexandria’s labs operate as production infrastructure for science rather than discretionary offices. VICOM collects the small tolls a city already needs, and the OBU rollout adds work that will echo into future inspections. These models improve by surviving.

Another thread is durable embeddedness over near-term returns. The approach is to win the workflow first and price later. Daily utility raises switching costs, deepens engagement, and earns pricing power over time. Adoption leads revenue with a lag. Doximity illustrates this as free tools embed in clinical routines and reliance increases. CLINT’s tenants are builders of code and process whose work follows talent and connectivity, not tariffs. Capacity in data centres fills because it is useful, and sustained use supports economics that justify expansion.

Stewardship of capital is the third strand. When the price of money is uncertain, flexibility matters more than forecasts. The task is to keep funding stable, resolve problems, and let channels reopen on their own clock. Arbor is doing the unglamorous work of provisioning and securing term non-recourse financing so that refinancing and gain on sale can resume without strain. Genting Singapore accepts near term disruption to fund long lived attractions from a strong balance sheet, trading noise today for durable cash flows tomorrow.

Geopolitics and policy will remain noisy and episodic. That is the surface. Underneath, households still seek leisure, researchers still need labs, cities still require testing and inspection, enterprises still centralize knowledge work, and clinicians still adopt tools that remove friction. These are slow, cumulative forces that do the bidding of time, guided by the simple discipline of choosing duration over drama. Keep balance sheets that do not force decisions at bad moments. Return surplus cash rather than chase empire. Accept that market perception moves in steps while business value moves in a line.

What follows is a review of these names previously covered.

CapitalLand Indian Trust (SGX:CY6U)

The half-year numbers show a business that continues to compound quietly. Distributable income grew 10% year-on-year, and DPU rose 9% (3.97 vs 3.64 cents). Against 2H FY2024, the rebound looks stronger still, with DPU up 24%. Not dazzling, but durable.

Occupancy stands at 90%. This is healthy, though not yet the mid-90s achieved by the leaders. Rent reversion of +9% confirms demand, and in a market where Global Capability Centres are expanding, there is a tailwind. Peer comparisons show room to climb, and mid-90s would command a premium multiple.

Leverage-wise, gearing sits at 42.3%, trimmed to 40.1% post-perpetuals. This is well within the regulatory ceiling but higher than some peers. Debt costs average 5.9%, buffered by 77% fixed rates. The balance sheet is not fragile, but vigilance remains necessary should refinancing collide with higher-for-longer rates.

The tenant base deserves more reflection than the filings allow. Much of the income is tied to US corporates, especially in technology and financial services. Some fear tariffs or shifting alliances might dull that demand. Yet CLINT’s tenants in India are not exporters of goods but producers of code, analytics, and research. Tariffs on steel or textiles do not unsettle a bank’s global back-office in Hyderabad. And geopolitically, while India charts its “strategic autonomy,” it should not preclude a US-India partnership that supports stability amid shifting power centres. Frictions over oil or tariffs should be manageable skirmishes in a broader alignment.

Management keeps distributions steady, a balance sheet that leans cautious, and the optionality of data centres. The first revenues from Navi Mumbai data centre Tower 1 arrive in the second half. Risks remain in occupancy, refinancing, and execution, but the foundations of recurring cash and long leases hold.

What the market sometimes misreads as fragility is, in fact, patient income compounding in a geography whose strategic importance only grows.

The original thesis can be accessed here: Initial report (7 May 2025)

Alexandria Real Estate Equities (NYSE: ARE)

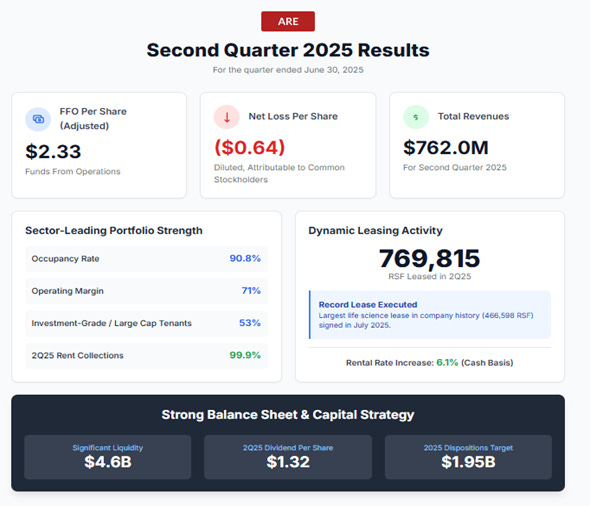

Alexandria’s second-quarter report reads as one more turn of the wheel in a familiar pattern. The company goes quietly about its business, while the market continues to treat it as if it were just another REIT caught in sectoral headwinds. Yet behind the noise, the facts accumulate.

Funds from operations remain steady, with $2.33 per share this quarter and $4.63 for the half year. Occupancy is high, and rents on renewed space rose 5.5% cash basis for the quarter. Such spreads are not the marks of a distressed landlord. They are the signs of scarcity in critical infrastructure that are the laboratories and not office blocks. The tenants which include global pharmaceutical firms and well-funded biotechs, treat these spaces as mission-critical.

That pattern was underlined in July, just after quarter-end, when Alexandria executed the largest life science lease in its history. A 16-year build-to-suit agreement with a multinational pharmaceutical tenant for nearly half a million square feet at its Campus Point Megacampus. Had this transaction been included in the second quarter, leasing volume would have risen to 1.2 million square feet, compared to the 770,000 reported. The event sits in “subsequent events” in the release, but it is worth drawing forward as it speaks to demand that is both durable and growing.

The balance sheet is strong, with largely fixed-rate debt, and a sizeable pipeline of new projects, much of it pre-leased. Growth, in other words, is already embedded. This is how resilient franchises behave. Quietly laying bricks that will pay rent long into the future.

The market’s story is oversupply. Alexandria’s story is pricing power. The distinction matters. At times like this, valuation gaps open between perception and reality. These are the moments when discipline is tested.

The temptation is to view every company through the prism of today’s cycle. But for a company with durable assets, high-quality tenants, and a record of compounding over time, patience is not only a virtue but a source of return.

The original thesis can be accessed here: Initial report (22 May 2025)

Arbor Realty Trust (NYSE: ABR)

Arbor describes 2025 as a transitional year and the numbers bear that out. Distributable earnings came in at $0.25 per share, $0.30 if adjusted for one-offs, while the dividend was reset to $0.30 to better match the current earnings power. Loan delinquencies are easing, but Real Estate Owned (REO) has risen as troubled loans move through foreclosure. That weighs on the income statement in the short run but leaves the balance sheet cleaner.

Funding has been steady and deliberate. A $500 million unsecured debt issue refinanced convertibles and added liquidity. Meanwhile, a ~$800 million build-to-rent (BTR) securitization locked in long-term, non-recourse funding for the single-family rental (SFR) platform. Net interest spread narrowed to about 1.08%, pressuring earnings, though even a modest rate decline could reopen refinancing opportunities. Management expects as much as $2 billion of agency originations next quarter.

On the agency side, elevated and volatile rates continue to dampen transaction and refinancing activity, lowering fee and servicing income. Delinquencies in Government-Sponsored Entity (GSE) loans have ticked up from recent lows but remain below long-term averages. Arbor’s $33.8 billion servicing portfolio still requires provisions, keeping investor sentiment cautious. Federal Housing Finance Agency (FHFA) lending caps have been supportive so far. A tighter stance would weigh on this capital-light business.

In structured lending, higher rates are putting pressure on borrowers, driving more loan modifications and foreclosures. Some earnings are being pulled forward into provisions, while other loans move into REO status until resolved. Unlike peers who are loosening standards to chase volumes, Arbor has stuck to discipline. That may hold back near-term growth, but it also protects spreads and credit quality. With property valuations lower, loan-to-values (LTVs) are higher, which means Arbor will likely need to build additional reserves.

Looking ahead, there are clear tailwinds if rates decline. Arbor’s $11.6 billion bridge loan book would benefit from refinancing, unlocking gain-on-sale income and boosting future servicing cash flows. FHFA’s focus on workforce and affordable housing plays directly to Arbor’s strengths.

Market dislocations should also create opportunities. Foreclose when needed, recapitalize with stronger sponsors, and re-originate loans on better terms. The SFR/BTR channel is a second growth leg, now supported by efficient securitization funding. Arbor’s broader access to capital via unsecured debt and fresh BB ratings also eases maturity management and diversifies funding.

The portfolio remains concentrated in the Sunbelt, with about a quarter in Texas and the mid-teens in Florida, primarily in workforce multifamily (Class B/C). While this avoids oversupplied luxury markets and helps sustain occupancy, local challenges remain with San Antonio and Houston facing weaker tenant demand, higher insurance costs in Florida, and elevated property taxes in Texas. Management characterizes these as transitional however.

Key items to watch include ongoing litigation (a class action and DOJ probe, both denied by management, who have signaled confidence with insider purchases in Q2 2025), macro risks, and borrower concentration. On the other side of the ledger, Arbor has about $600 million in liquidity and generates roughly $126 million in annual servicing cash flow, providing ballast while REO is resolved and originations rebuild.

No doubt Arbor is in the trough, with earnings compressed, and the dividend reset, while credit clean-up is ongoing. But the pieces for recovery are in place. A stronger balance sheet, broader funding options, a Sunbelt/workforce focus, and a scalable SFR/BTR platform.

If rates fall, agency volumes and refinancing lead the rebound. Servicing, spreads, and earnings follow, and distributions rise again. If rates stay high, the balance sheet work and funding flexibility buy Arbor time.

The nature of the credit business requires patient capital willing to sit through the turn.

The original thesis can be accessed here: Initial report (31 May 2025)

VICI Properties (NYSE: VICI)

VICI’s second quarter was another exercise in doing what it always does. Collecting rent, raising guidance, and showing that a simple business model, well executed, compounds quietly over time. The market may still think of it as a gaming landlord, but the evidence is clear that the company’s role is broader.

Net income came in at $865 million, with AFFO at $0.60 per share. Management raised full-year guidance to as much as $2.37 per share. Revenues grew 4.6%, not through dramatic expansion but through the slow machinery of contractual escalators and new investments. The portfolio is fully occupied, with a weighted average lease term of over forty years. Debt is largely fixed, and leverage is moderate.

The strategy remains consistent. Capital is recycled into high-quality projects like One Beverly Hills and North Fork Casino, while non-core assets are pruned. The model is functioning as designed. Long leases, CPI-linked escalators, and inflation-protected growth. If there is risk, it lies in tenant concentration, with Caesars and MGM still accounting for most of the rent. Yet all obligations are met, and the balance sheet leaves room for optionality.

The market continues to value VICI as if it were a conventional REIT, vulnerable to cycles. But the long-dated cash flows, full occupancy, and embedded growth supports a strong distinction.

On these measures, VICI remains a steady place to hold capital when markets move.

The original thesis can be accessed here: Initial report (14 Jun 2025)

Doximity (NYSE: DOCS)

Doximity opened its fiscal year with strength. Revenues rose 15% to $146 million, net income reached $53 million, and free cash flow grew by more than half. Margins widened further, with adjusted EBITDA climbing to $80 million at a 55% margin. The balance sheet is clean, with $841 million in cash and little debt. By any financial measure, this is a business in command of itself.

More revealing are the patterns beneath the numbers. Existing customers expanded their spending with net revenue retention at 118% while the number of clients contributing over $500,000 annually continued to grow. These are signs of a platform becoming more deeply embedded in the fabric of healthcare.

The company’s new chapter is in artificial intelligence. Tools like AI Scribe and the newly acquired Pathway Medical are being offered free, designed to integrate into the daily routines of physicians. Weekly engagement already exceeds 75%. This is less a revenue story today than one of utility. If physicians come to rely on these tools, monetization will follow.

The risk lies in timing. Free tools build engagement but delay cash returns. Stock-based compensation is rising with acquisitions, and growth in net revenue retention has softened slightly. These are not trivial, but they are also not thesis-breaking.

The thesis remains. Doximity is a rare network with high profitability, strong cash generation, and an expanding role in physician workflows. The earnings confirm it. The market still values Doximity mainly as a digital marketing channel. Over time, it may come to be valued as infrastructure for the medical profession.

An investor’s task here is to own the time between how the market labels Doximity and what the product is becoming.

The original thesis can be accessed here: Initial report (23 Jun 2025)

Genting Singapore (SGX: G13)

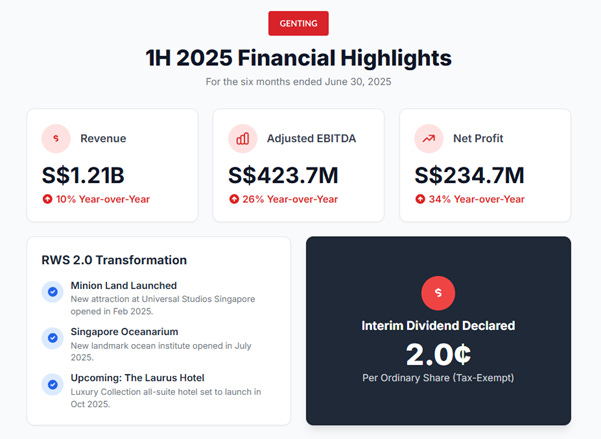

Genting’s half-year results look poor at first glance. Revenue fell to S$1.21 billion, profit dropped 34% to S$234.7 million, and margins narrowed. The cause is neither cyclical nor structural decline, but by design. Genting has chosen to wound the present to enlarge the future. The S$6.8 billion RWS 2.0 expansion is tearing up familiar ground so that something larger may grow. Like any major works, the noise and dust obscure the shape of what is coming.

Gaming, the cash engine, fell 12% likely due to the drop off from 2024’s initial visa-driven demand. Non-gaming was steadier, helped by the launch of Minion Land. Yet new rides cannot fully mask the closure of an aquarium or the scaffolding around a resort. EBITDA down 26% tells the same story, that this is a bridge year.

The other side of the ledger looks different. Genting carries S$3.32 billion in cash and little debt. Even amid disruption, operations generated S$369 million of cash. Capex is rising fast, but it is funded from a fortress balance sheet. Where some operators build castles on borrowed sand, Genting builds from granite.

Management’s narrative is consistent with prior commentary. RWS 2.0 will deliver a new Singapore Oceanarium, a WEAVE precinct, and the Laurus hotel. Early proof lies in Minion Land’s successful opening. The dividend was maintained, a small but clear signal that future cash flows are expected to return.

However, risks remain to the uncertainty on what patience can buy. Execution of a multi-year expansion is no small feat. Costs could creep, margins may lag, or regulators could remain skeptical after shortening the license renewal. Gaming revenues will always be volatile. Yet none of this undermines the core thesis that the business is a duopoly in Singapore, funded with net cash, investing heavily into long-lived attractions that aim to pull global travellers into its orbit.

This is not a “beat and raise” stock, but a long-duration compounding machine rebuilding its foundation. Investors should not mistake the bridge for the destination. If one believes in the draw of Singapore as a tourism hub in 2040, then this year’s discomfort is the price of admission.

The original thesis can be accessed here: Initial report (2 Jul 2025)

VICOM (SGX: WJP)

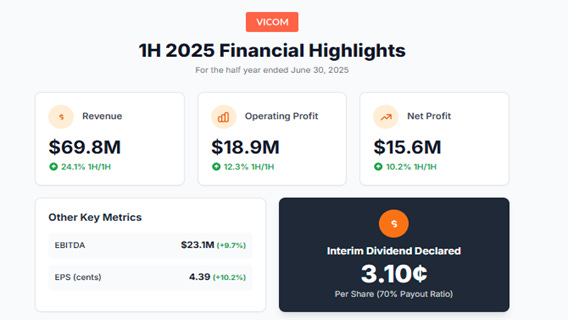

VICOM’s first-half results confirm what the original assessment. The business is sturdier than the market credits, and the ERP 2.0 On-Board Unit (OBU) installation has lit the short-term fuse. Revenue rose 24%, profits less, reflecting the project’s lower margin profile. None of these surprises. The project is a sprint layered onto a marathon.

It is worth remembering that this is not a company reinventing itself, but a company collecting the tolls that already exist, plus one more. The OBU programme, now two-thirds complete, is temporary in installation but permanent in legacy. A million devices out in the field mean future work in diagnostics, maintenance, and integration into inspections. A short sprint leaves a long tail.

Margins compressed because subcontractor costs rose, not because the core franchise weakened. Vehicle inspections remain profitable, SETSCO quietly expands alongside Singapore’s construction and manufacturing needs, and management continues to recycle windfalls to shareholders rather than chase empire. The interim dividend at a 70% payout ratio speaks louder than any strategy discussion.

More interesting than today’s project is tomorrow’s tide. Singapore’s 2030 deadline on new ICE car registrations has shifted incentives. Most owners will likely renew COEs, not replace. As COEs are extended, the fleet ages. And with age comes more frequent inspections, every year instead of every two. By the decade’s end, assuming ~70% renewal rate, nearly half the car population will require annual inspection. That is a structural boost to VICOM’s highest-margin business, that market may be ignoring.

Some worry about the earnings cliff after installations conclude. While a fair concern, there are two mitigating considerations. First, the underlying businesses continue to grow, as confirmed by management’s note on testing volumes. Secondly, the OBU wave generates excess cash which is flowing straight back to investors.

The lesson is that markets often overvalue the visible project and undervalue the invisible current beneath. One should stay the course, not for the boom of today, but for the wave that follows.

The original thesis can be accessed here: Initial report (17 Jul 2025)

Earnings Notes is important!

I write about the stock market from both a fundamental and technical analysis perspective. I cover the US, Hong Kong, and Malaysia stock markets daily.

kingkkk.substack.com

Great post!